How to Detect and Prevent Synthetic Identity Fraud

Key Takeaways.

1. Synthetic identity fraud is a sophisticated and costly threat that requires proactive measures to detect and prevent.

2. Understanding how synthetic identities are created and recognizing the red flags, businesses can stay one step ahead of fraudsters.

3. Implementing preventive mechanisms and leveraging trusted solutions like artificial intelligence and machine learning algorithms are essential in mitigating this risk.

What is Synthetic Identity Fraud?

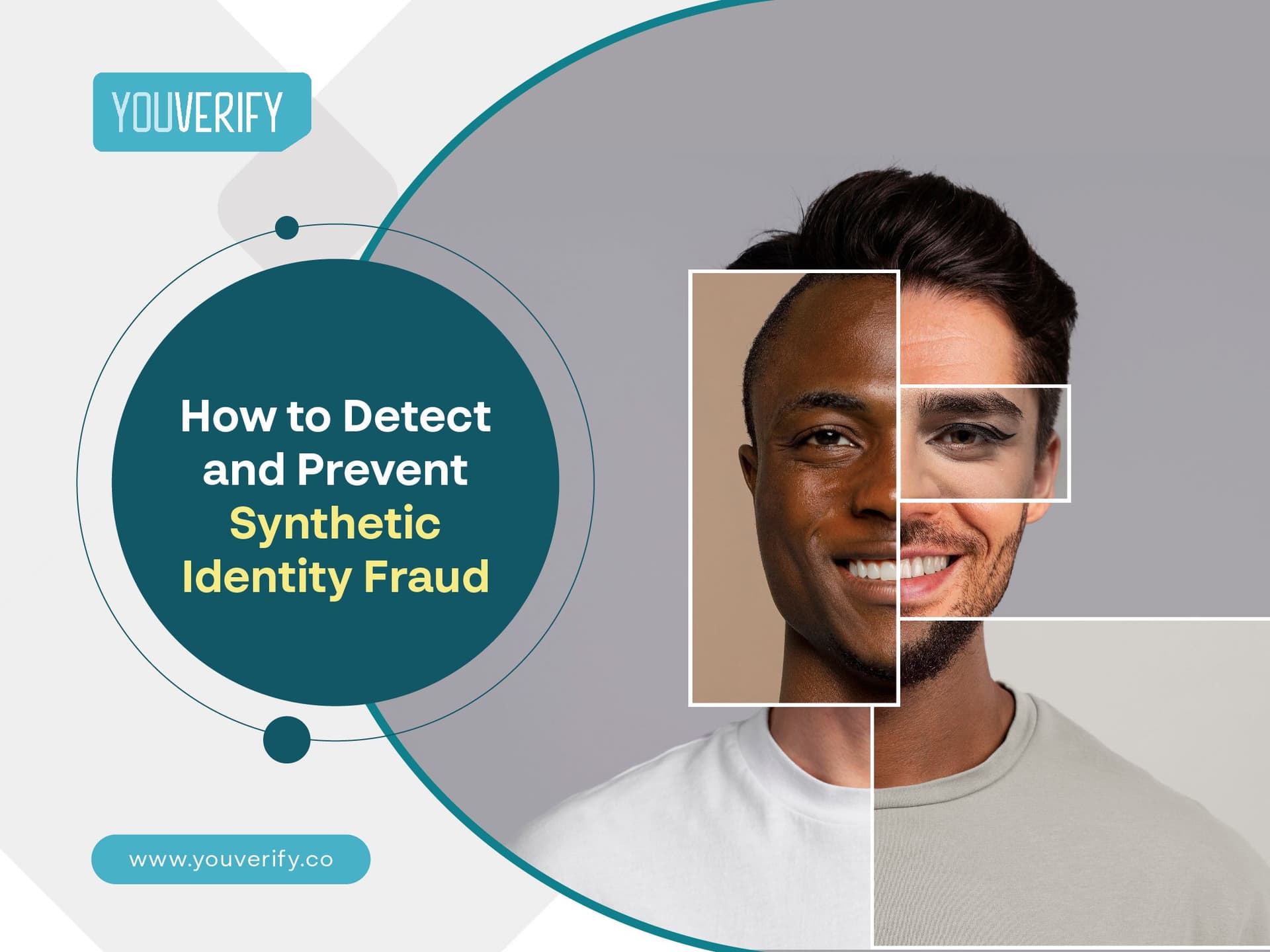

Synthetic identity fraud is a type of fraud in which criminals create a fake identity by combining real and synthetic credentials to create a new and fictitious identity. This information includes Social Security numbers (SSNs), names, addresses, and dates of birth.

Synthetic identity fraud involves using a real person's real information to create a new identity that only exists in the digital system, making it difficult to detect. These false identities are used by fraudsters to open bank accounts, apply for credit, launder money, or engage in other illegal activities.

In the first half of 2024, synthetic identity fraud had a 7% increase rate of losses. The average value of synthetic identity fraud losses from banks is $15k, and it is projected to have a $23 billion loss by 2030. Identity fraud is more than a present challenge; it is a future one, and requires the urgency of immediate security measures.

In this article, we are going to be looking into how to detect and also prevent synthetic identity fraud.

Understanding how synthetic identity fraud happens.

Synthetic identity fraud is a progressive, multi-layered crime wherein the criminal mixes stolen personal data, such as Social Security numbers or tax identity numbers, with created information, like fictitious names, addresses, and dates of birth.

The real information is usually hacked through breaches, phishing attacks, or dark-web markets, after which this information is combined with created data to make up a new identity that does not actually exist.

The fictitious identity is further used to apply for credit or any financial product. Although this particular identity might get declined initially, repeated attempts slowly build up a thin credit profile.

Once the fake identity has matured to the level where it may pass basic verification checks, it is used as a tool for committing major fraud, such as securing large loans, opening credit lines, or making high-value transactions before disappearing.

This long, meticulous process makes synthetic identity fraud challenging to detect at the earliest stage and highlights how easily one or more steps can go awry.

How to identify Synthetic Fraud

1. Unsecured debts

It has been observed that synthetic identity fraud is mostly tied to large amounts of unsecured debts. These debts can be credit card balances or personal loans, which do not require much documentation to acquire. If you notice a rise in the person's unsecured debt, take it as a sign that he or she may be using a synthetic identity.

2. Multiple credit requests at a short time

This is mostly due to their impatience in building a credit profile that they can exploit and submitting multiple credit applications within a short period of time. When you find out that multiple lenders are making inquiries on a particular identity, it's most likely that it's a synthetic one.

3. No correlation between the age and credit history

When you notice an account holder is younger than his credit history shows, it is most likely that the identity is a synthetic one set up by a criminal to exploit the system. An example is having a 25-year-old account holder with a credit history of 20 years. One can't start taking credit since he was five. Flag it; it's most likely a synthetic identity.

4. Suspicious Mailing Address

If you notice identities using a temporary address for a transaction that has been used by multiple identities, that is a red flag; it may be used by a synthetic identity fraudster. These temporary addresses could be virtual mailboxes, P.O. boxes, or residential addresses.

5. Similar or Matching Contact Information

If you notice that multiple identities are sharing the same phone number, email address, or residential address, flag it; it may just be one of the multiple synthetic identities used by a fraudster.

6. Matching social security numbers

You can also set parameters to look out for matching social security numbers used across multiple accounts under different names or residential addresses. This can tell if a synthetic identity fraudster is on the prowl.

How to Prevent Synthetic Identity Fraud

Preventing synthetic identity fraud for business includes the following:

1. Use Advanced Identity Verification Technology

Identity verification tools help businesses confirm a person's identity during customer onboarding. Implement biometric verification checks such as facial recognition and fingerprint scanning, and enforce multi-factor authentication that ensures users provide two or more verification factors.

2. Follow a Two-Step Verification Process

Incorporating a two-step verification process can help businesses prevent synthetic identity fraud. Implementing government-issued identity checks for anomalies in their security features, like holograms and microtext. Also, a liveness check that mandates the customer to submit a real-time selfie, asking them to blink, smile, or open their mouth for verification.

After getting this verified, the system would then cross-reference all the information gotten instantly against public and proprietary databases like credit bureaus, utility records, voter registries, and others to see if the person involved is a real-life person.

3. Fast fraud detection technology

Use tools learning to detect and automatically flag usual patterns in account activities, such as large transactions or rapid fund movement that may indicate fraud, and monitor the behavior of account holders

FAQ’s

1. What is synthetic identity fraud?

Synthetic Identity fraud is the creation of a whole new identity that is not associated with a real person, using fabricated credentials

2. Why is synthetic identity fraud hard to detect?

Synthetic identity fraud is hard to detect because the created fake identities can pass standard onboarding checks.

3. What are the common examples of fraud?

Common fraud schemes that target customers include identity theft, non-delivery scams, online car buying scams, and theft of debit and credit cards.

Prevent Synthetic Identity Fraud with Youverify

As technology advances, manual verification processes are time-consuming and prone to human error. Automating identity verification with trusted solutions streamlines the process and improves accuracy.

At Youverify, we provide real-time identity verification solutions that help businesses authenticate customers' IDs in seconds. We also provide biometric and liveness checks to ensure that all your customers are genuine individuals and not deepfakes or static images used by scammers.

Our solution ensures organizations detect suspicious activities using artificial intelligence and machine learning algorithms, making Youverify the right partner for businesses looking to safeguard their operations from synthetic identity fraud.

Make Youverify a partner to help your business fight fraud and maintain compliance seamlessly. Book a free demo today.

Related Articles

Fraud Detection Using Machine Learning - How Does it Work?

What is Bank Fraud with Examples