In today's global financial landscape, businesses must remain vigilant against illicit activities, such as money laundering, terrorist financing, and fraud. To ensure transparency and maintain the integrity of the financial system, Know Your Business (KYB) compliance has become a crucial practice in the financial industry. KYB compliance goes beyond just knowing the customer; it involves understanding the structure and beneficial ownership of business entities.

This step-by-step guide aims to equip financial institutions with the knowledge and tools to effectively implement KYB compliance processes, leveraging technology and best practices to stay ahead of emerging risks.

I. Understanding KYB Compliance

Lets look at some key definitions and terminologies of KYB:

A. Definition and Objectives of KYB Compliance

Know Your Business (KYB) compliance refers to the process of verifying the legitimacy and beneficial ownership of business entities before engaging in financial transactions. The primary objective is to identify and mitigate risks associated with potential criminal activities, including money laundering and financing of terrorism. KYB compliance plays a vital role in safeguarding financial institutions and the global financial system.

B. Regulatory Landscape and Authorities Governing KYB Compliance

Financial institutions must be well-versed in the regulatory landscape governing KYB compliance. Key authorities such as the Financial Action Task Force (FATF) provide guidelines and standards to combat money laundering and terrorist financing. Regional Anti-Money Laundering (AML) directives and other relevant regulations also play a significant role in shaping KYB compliance practices.

C. Why it is Importance for Financial Institutions to Implement KYB Compliance

For financial institutions operating in today's heavily regulated environment, understanding and implementing KYB compliance is not optional but mandatory. Non-compliance with KYB requirements can lead to severe consequences, such as reputational damage, financial penalties, and a loss of customer trust. Embracing KYB compliance is a proactive measure that strengthens an institution's risk management framework and enhances its reputation.

II. Preparing for KYB Implementation

A. Conducting a Thorough Risk Assessment

The first step in implementing KYB compliance is conducting a comprehensive risk assessment. Financial institutions must identify and analyze the potential risks associated with their customer base, products, and geographic locations. A risk assessment allows organizations to allocate resources effectively and prioritize high-risk entities that require more rigorous due diligence.

B. Assembling a Dedicated KYB Compliance Team

To ensure the success of KYB compliance, financial institutions should assemble a dedicated team or assign responsibilities to individuals with expertise in Anti-Money Laundering (AML), Counter-Terrorist Financing (CTF), and KYB regulations. This team will be responsible for overseeing the KYB implementation, conducting ongoing monitoring, and keeping abreast of regulatory changes.

C. Allocating Resources and Budget for Implementation

Effective KYB compliance requires adequate allocation of resources and budget. Financial institutions must invest in technology, training, and expert consultation to streamline the KYB process and ensure continuous compliance monitoring.

Further reading Steps to Establish an Effective Business Verification KYB Process

III. Conducting Business Verification Checks

A. Importance of Business Verification in KYB Compliance

Business verification is the foundation of KYB compliance. It involves verifying the legal existence and legitimacy of the business entity. Financial institutions must ascertain that the business operates lawfully and transparently, without any involvement in illicit activities.

B. Validating Registration Documents, Licenses, and Certifications

To verify the authenticity of the business entity, financial institutions should collect and validate essential documents, such as business registration certificates, licenses, and certifications. These documents provide crucial insights into the legitimacy of the business and its operations.

C. Performing Adverse Media Screening for Reputation Assessment

In addition to verifying official documents, financial institutions must conduct adverse media screening to assess the reputation and history of the business. Adverse media screening involves searching public records, news articles, and other sources for any links to criminal activities or negative press associated with the business. By performing this screening, financial institutions can identify potential risks and make informed decisions regarding their customer relationships.

IV. Risk Assessment and Customer Categorization

A. Developing Risk Assessment Criteria for Different Business Entities

Every business entity poses varying levels of risk, depending on factors such as industry, location, and transaction volume. Financial institutions must develop risk assessment criteria tailored to different types of businesses. These criteria help in categorizing customers based on their risk levels, allowing institutions to apply appropriate due diligence measures.

B. Identifying High-Risk Entities Requiring Enhanced Due Diligence

As part of risk assessment, financial institutions must identify high-risk entities that warrant enhanced due diligence. These high-risk entities may include politically exposed persons (PEPs), businesses in high-risk jurisdictions, or those involved in high-value transactions. Enhanced due diligence ensures thorough investigations into the ownership, financial history, and operations of these entities to understand associated risks fully.

C. Establishing a Risk-Based Customer Categorization System

Based on the risk assessment, financial institutions should establish a risk-based customer categorization system. This system helps prioritize ongoing monitoring efforts, allocate resources efficiently, and focus on high-risk customers. Implementing this system ensures that the institution's compliance efforts are targeted, proportionate, and risk-focused.

V. Implementing Ongoing Monitoring and Updating Processes

A. Importance of Continuous Monitoring in KYB Compliance

KYB compliance is not a one-time process but an ongoing effort. Continuous monitoring of customer activities and transactions is vital to detect any unusual or suspicious behaviour promptly. Financial institutions must establish systems for real-time monitoring to identify potential red flags and take immediate action when necessary.

B. Real-Time Monitoring of Business Activities and Transactions

Compliance solutions equipped with real-time monitoring capabilities play a pivotal role in KYB compliance. These solutions allow financial institutions to stay alert to potential risks and suspicious activities as they happen. Real-time monitoring empowers institutions to respond swiftly to any emerging threats and take appropriate measures to mitigate risks.

Also, read what is Know Your Transaction (KYT) Compliance

C. Regular Updates and Re-Verification of Customer Information

To maintain compliance with evolving regulations and changes in business structures, financial institutions must regularly update and re-verify customer information. Business entities undergo continuous changes, such as ownership transfers, expansions, or mergers. These changes can impact the risk profile of the customer, necessitating periodic updates to ensure accurate risk assessments.

Updating customer information is not only a regulatory requirement but also a best practice to keep KYB compliance effective and up-to-date. Advanced compliance solutions automate this process, streamlining the updating and re-verification procedures for financial institutions managing a large volume of business clients.

VI. Leveraging Technology for KYB Compliance

A. Role of Technology in Streamlining KYB Compliance Processes

In the digital era, technology is a crucial ally for financial institutions seeking to optimize KYB compliance processes. Compliance solutions that leverage advanced technologies, such as artificial intelligence (AI), machine learning, and data analytics, streamline manual tasks, reduce human errors, and enhance the efficiency of KYB compliance.

B. Exploring and Investing in KYB Compliance Software Solutions

Financial institutions should explore and invest in specialized KYB compliance software solutions tailored to their needs. These solutions offer automated business verification, real-time monitoring, and ongoing customer data updates. By integrating these solutions with existing anti-money laundering (AML) and customer due diligence (CDD) systems, institutions can create a comprehensive compliance framework that ensures seamless integration of data across various compliance functions.

You might be interested in reading Benefits of Transaction Monitoring Software for Anti-Money Laundering

C. Integrating KYB Processes with Existing AML and CDD Systems

Effective KYB compliance requires a holistic approach that aligns with existing AML and CDD processes. Integrating KYB compliance with these systems enhances overall risk management capabilities and reduces duplication of efforts. A unified compliance framework ensures a consistent and coherent approach to customer due diligence, strengthening the institution's overall risk mitigation strategies.

VII. Training and Education

A. Importance of Educating Employees on KYB Compliance Procedures

Human capital is a critical component of KYB compliance. Financial institutions must invest in comprehensive training programs to educate employees about KYB compliance procedures, their importance, and the consequences of non-compliance. Training should encompass both front-line staff, such as relationship managers and compliance officers, and senior management, who play a significant role in setting the compliance tone and culture.

B. Conducting Comprehensive Training Programs and Workshops

Regular workshops and educational sessions keep employees updated on changing regulations and emerging trends in KYB compliance. These programs should provide practical examples and case studies to enhance understanding and practical application of KYB compliance principles.

C. Keeping Employees Updated on Changing Regulations and Trends

Regulatory requirements and best practices in KYB compliance evolve. Financial institutions should ensure that their employees stay informed about these changes through regular updates, seminars, and industry conferences. Staying updated ensures that the institution's KYB compliance efforts remain aligned with the latest standards and expectations.

VIII. Challenges and Best Practices

A. Common Challenges in Implementing KYB Compliance

Implementing KYB compliance may encounter various challenges, including resource constraints, data management complexities, and keeping pace with evolving regulations. Financial institutions may face resistance from customers during the due diligence process, requiring effective communication and transparency in explaining the rationale behind KYB compliance requirements.

B. Best Practices for Overcoming Challenges

To overcome these challenges, financial institutions should adopt best practices in KYB compliance implementation. Collaboration with industry experts and regulatory consultants can provide valuable insights and guidance on KYB best practices. Leveraging advanced technology solutions streamlines the KYB process and alleviates resource constraints while learning from successful case studies in KYB compliance implementation provides valuable lessons and strategies for managing challenges effectively.

C. Learning from Successful Case Studies in KYB Compliance

By analyzing successful case studies in KYB compliance, financial institutions can draw lessons from others' experiences and acquire valuable insights into best practices. By understanding how other organizations have successfully implemented KYB compliance, institutions can adapt and tailor these strategies to their unique circumstances and needs.

How to Achieve KYB Compliance with Youverify

We recommend that you leverage a engage reliable verification service provider to verify business addresses for swift operation.

Here, we will be taking you on a step-by-step journey on how businesses can perform business address verification using Youverify’s solution:

Step 1: Create an account and login to the Youverify platform

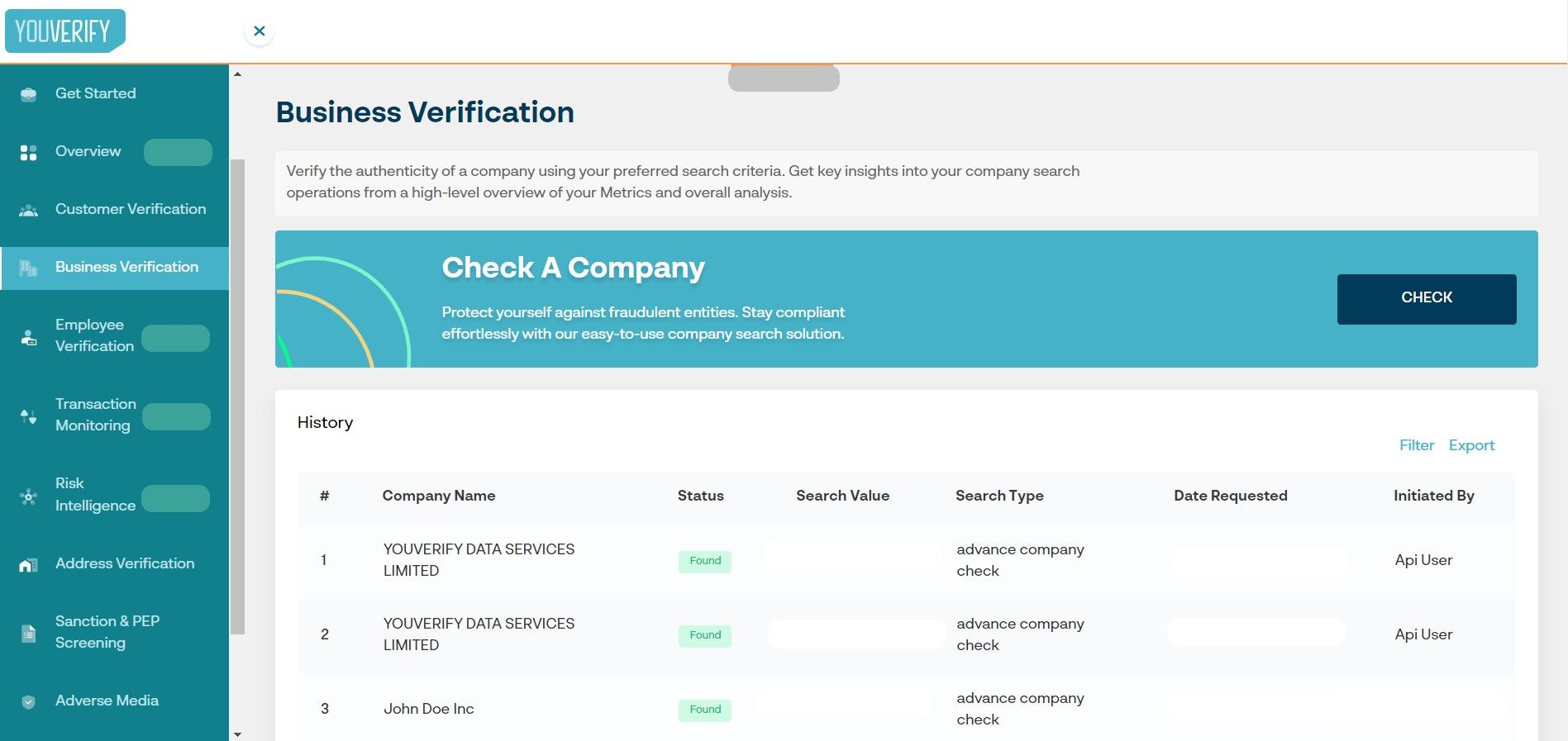

Step 2: Navigate to “Business Verification” on the left side of your home page

Step 3: Select “ Check”

Step 4: Select either “Company Search” (gives you basic company information) or “Advanced Company Search” (gives you elaborate information including details on shareholders and other affiliated entities)

Step 5: Fill up the requested information like “Country”, “Registration Number”, “Company Name”, etc and click “Search”.

The detailed business information will be revealed for you to make an informed decision on the business.

KYB compliance is a critical aspect of risk management for financial institutions, ensuring transparency and mitigating the risk of financial crimes. By following the step-by-step guide outlined in this article, financial institutions can effectively implement KYB compliance processes, leveraging technology and best practices to stay ahead of emerging risks.

Through continuous education and commitment to compliance, financial institutions can contribute to a safer financial ecosystem while building trust and maintaining a reputation for ethical and responsible business practices. Embracing KYB compliance as an essential part of their business strategy, institutions can navigate the evolving regulatory landscape with confidence, safeguarding their operations and customers alike.

Implementing KYB Compliance Processes using Youverify solutions will give you access to all your verification needs in one place.

See how 100+ leading companies use Youverify to Implement end-to-end KYB compliance. Request a demo today.